Online Loan Checkout

Improving the loan closing experience for merchants and documentation specialists through a new online platform, resulting in 85% less closing calls.

Lead UX Designer

Web & Mobile Experience

Credit

6 Months

Overview

Optimizing Loan Processing: Funding More Deals In Less Time

As the lead designer of this project, I created a new online process that would replace the need to call merchants for verification. This self-checkout experience allowed merchants to visit a link to verify their identity, review loan terms, and sign documents digitally before funding. Moreover, this project aimed to reduce the need for documentation specialists to get on calls and focus on other key responsibilities to move deals forward. Since launch, our partners and merchants have provided positive feedback and have expressed how useful this new online tool has been.

Responsibilities

Product thinking, UX analysis, wireframing, visual design, prototyping, quality assurance

Team

1 Designer, Chief Operating Officer (COO), Chief Credit Officer (CCO), 3 Developers, 1 QA Engineer

The Challenge

How might we facilitate the loan closing experience for merchants and prepare them for the funding phase efficiently?

The current process involves a scheduled call between a documentation specialist and a merchant in which a few verification questions are asked and loan terms are discussed. Since documentation specialists have to set a time for calls, these calls can interrupt their process. With this new self-sufficient process, the intention was to free up more time for documentation specialists to review stipulations of incoming deals and as a result, get more deals through the funding queue.

Solution Preview

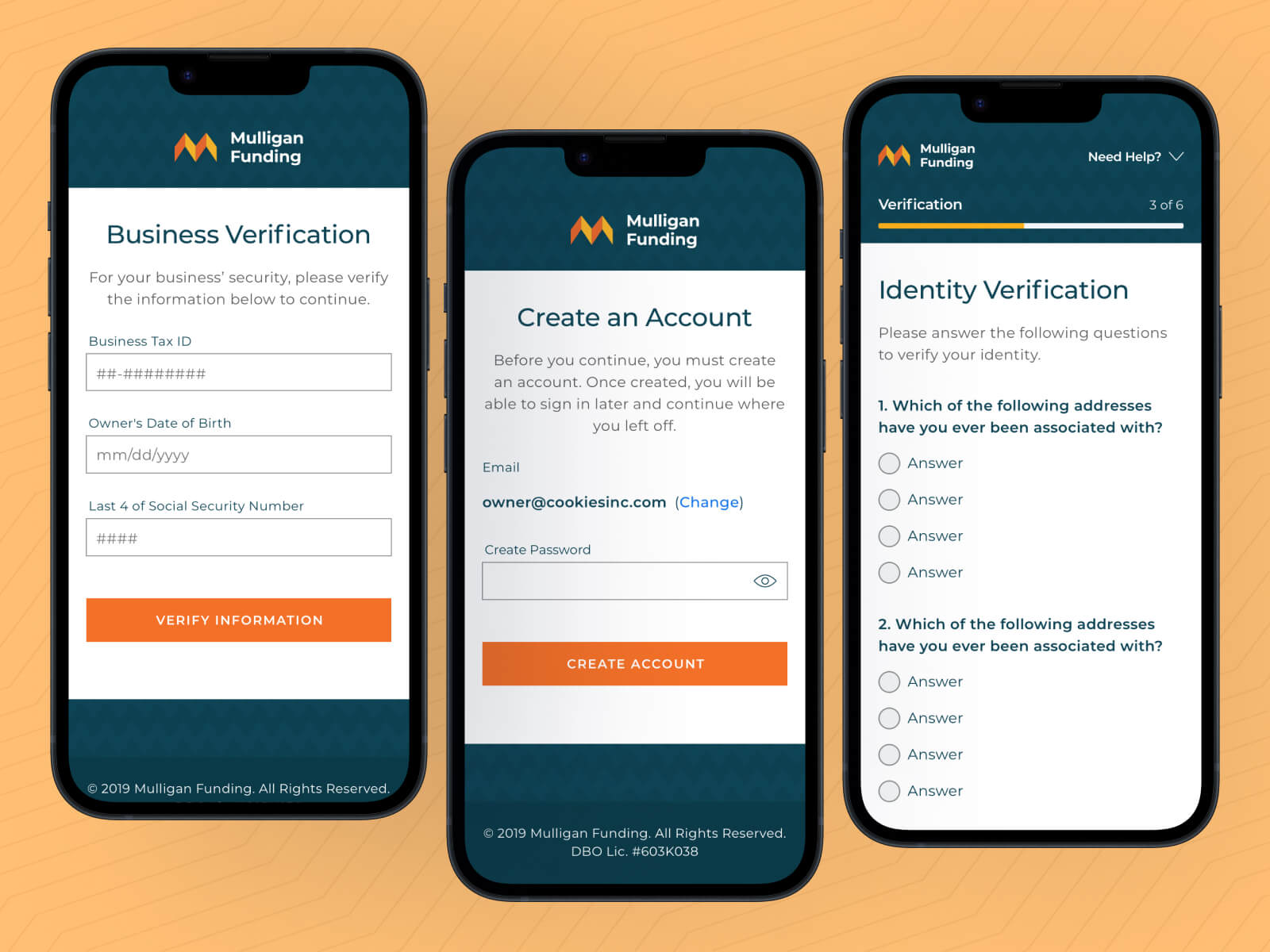

Verifying Business Information & Individual Identity

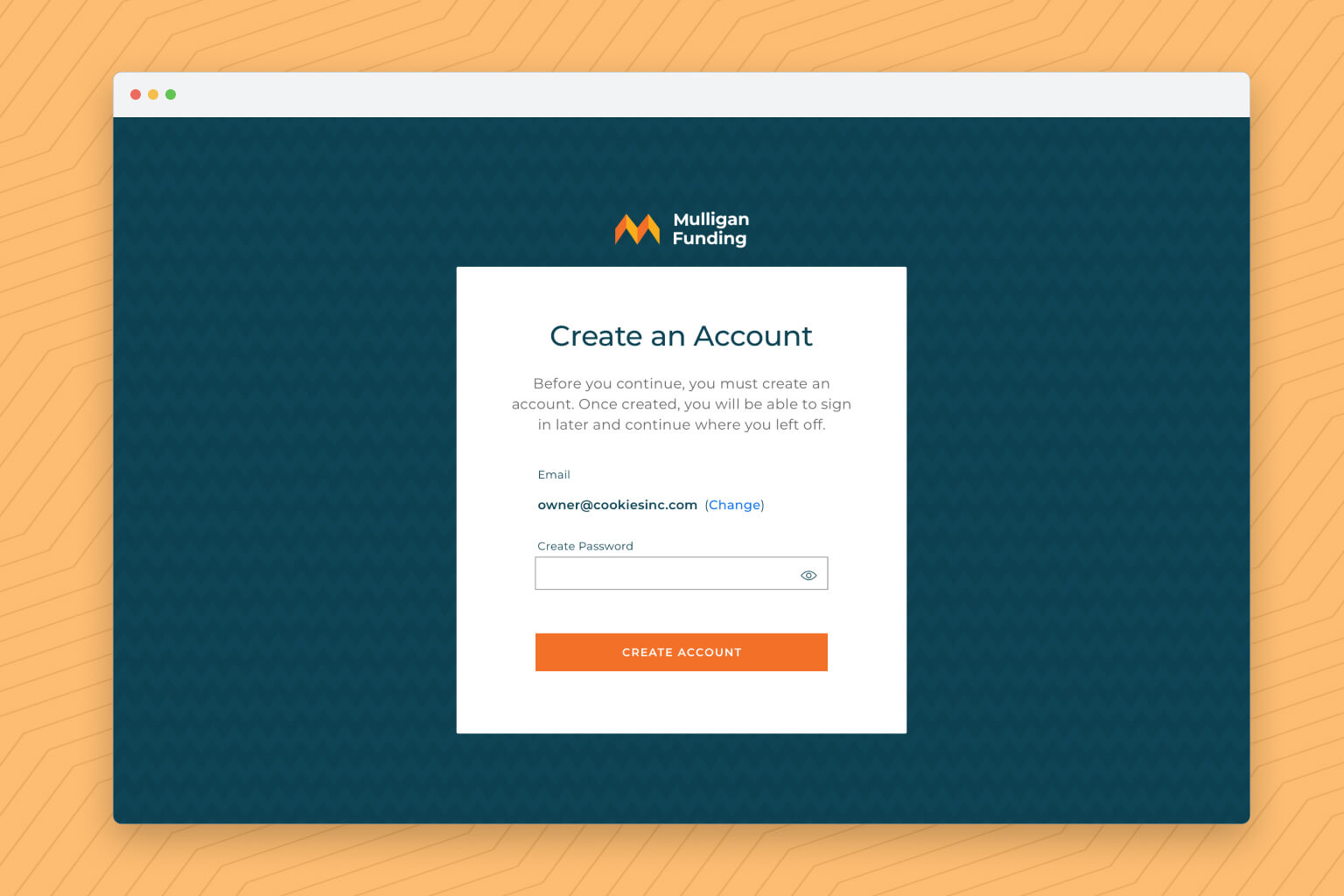

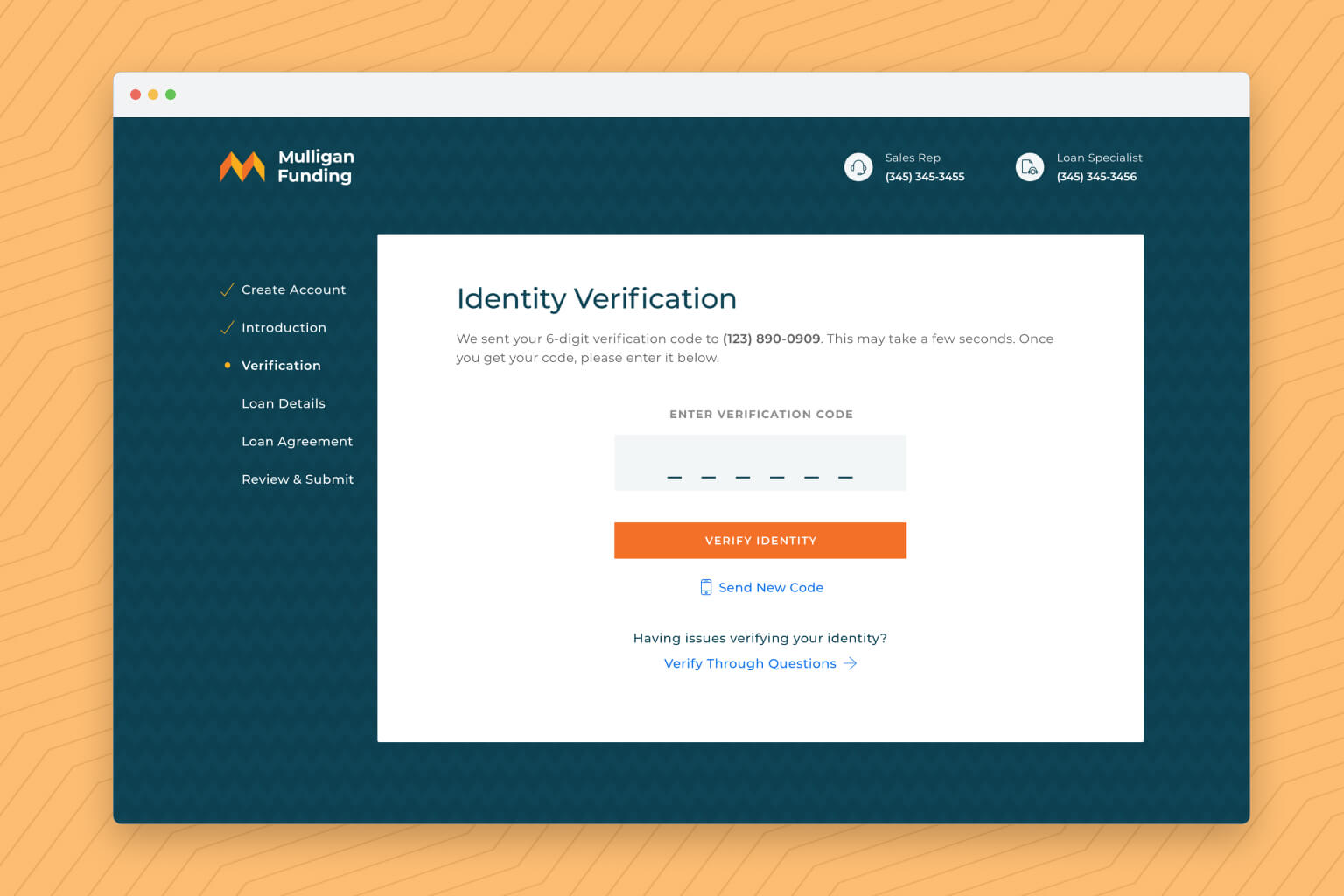

Business verification was added as a security step for owners to create an online account. Once an account is created, owners are asked knowledge-based authentication questions.

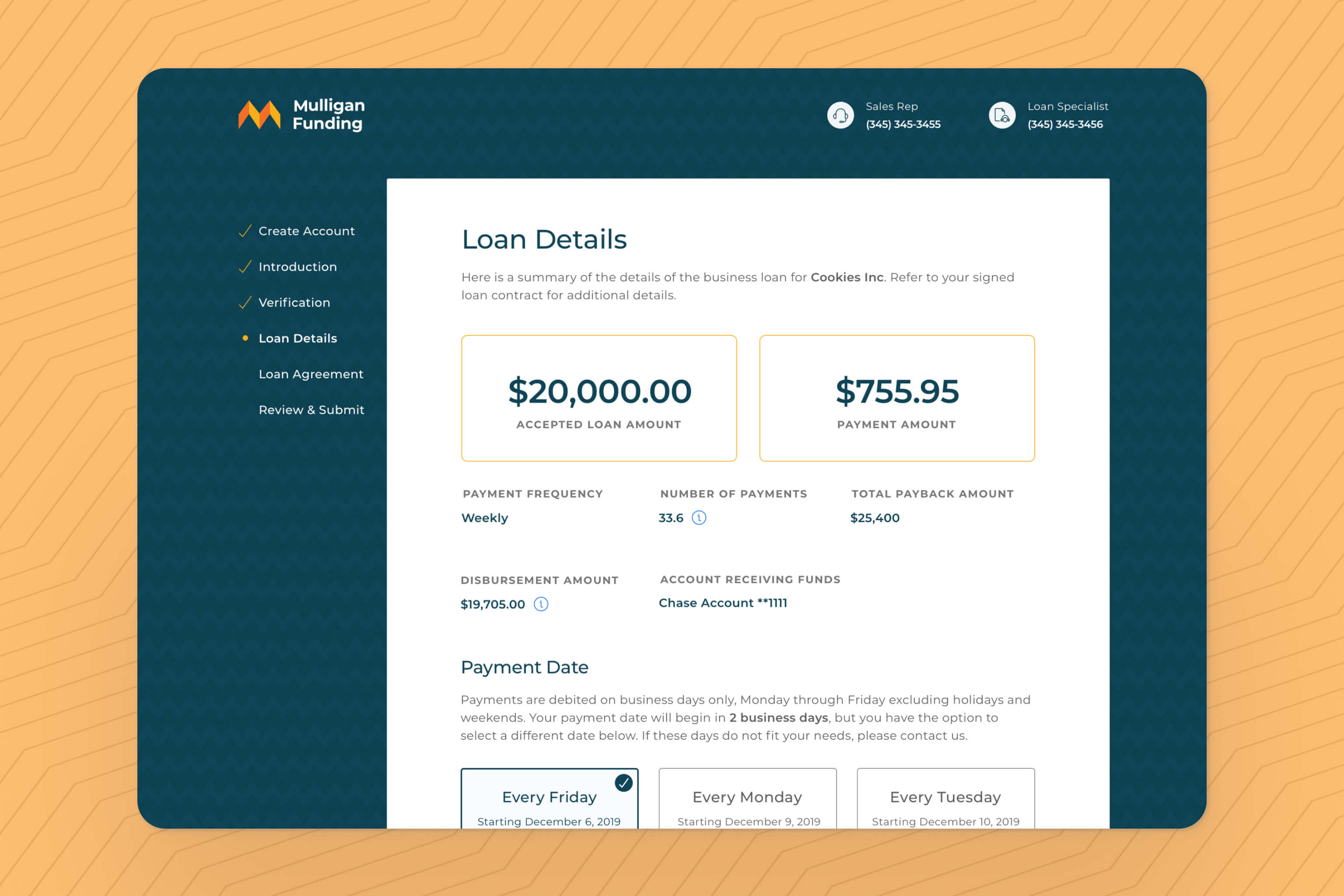

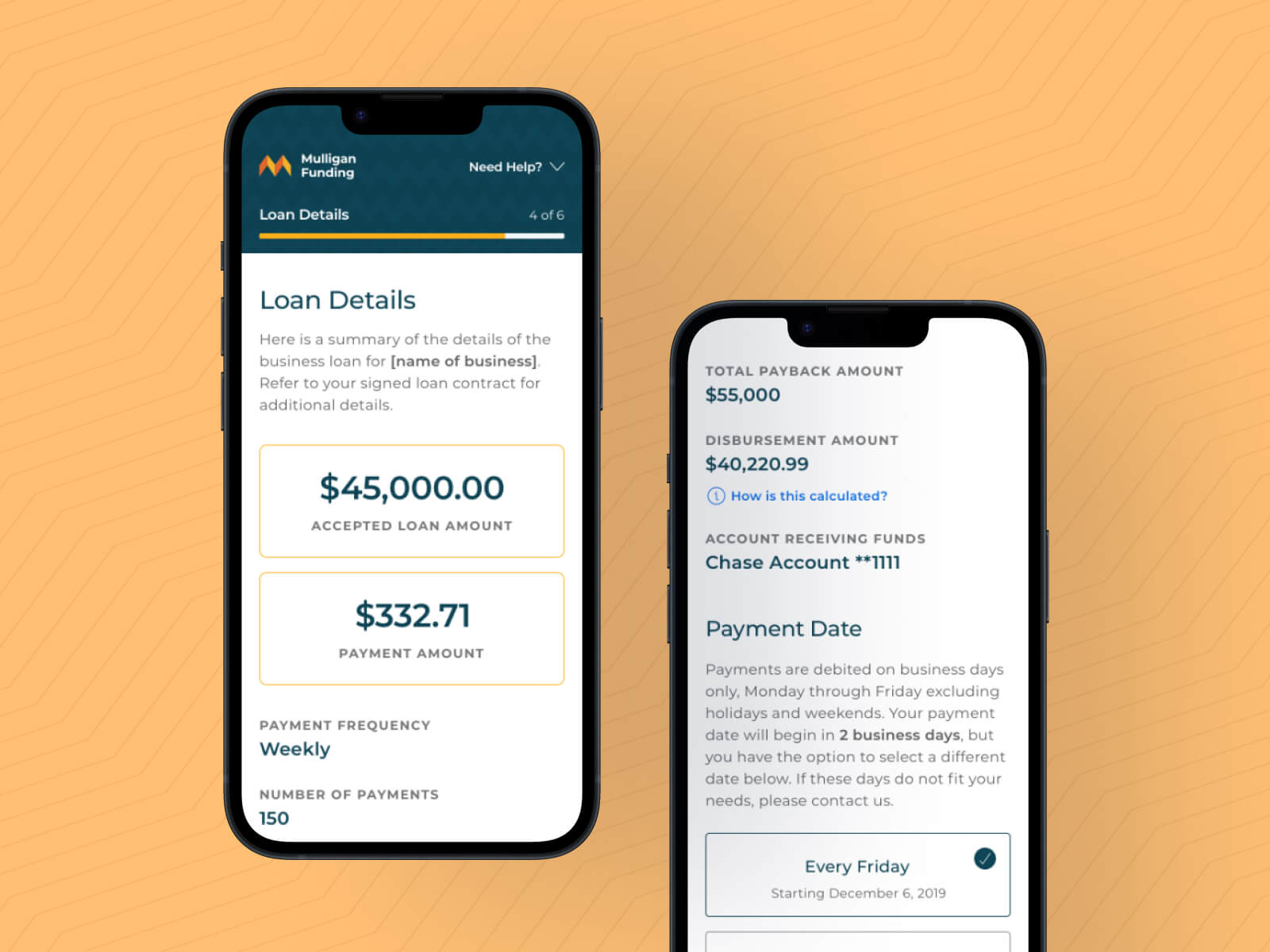

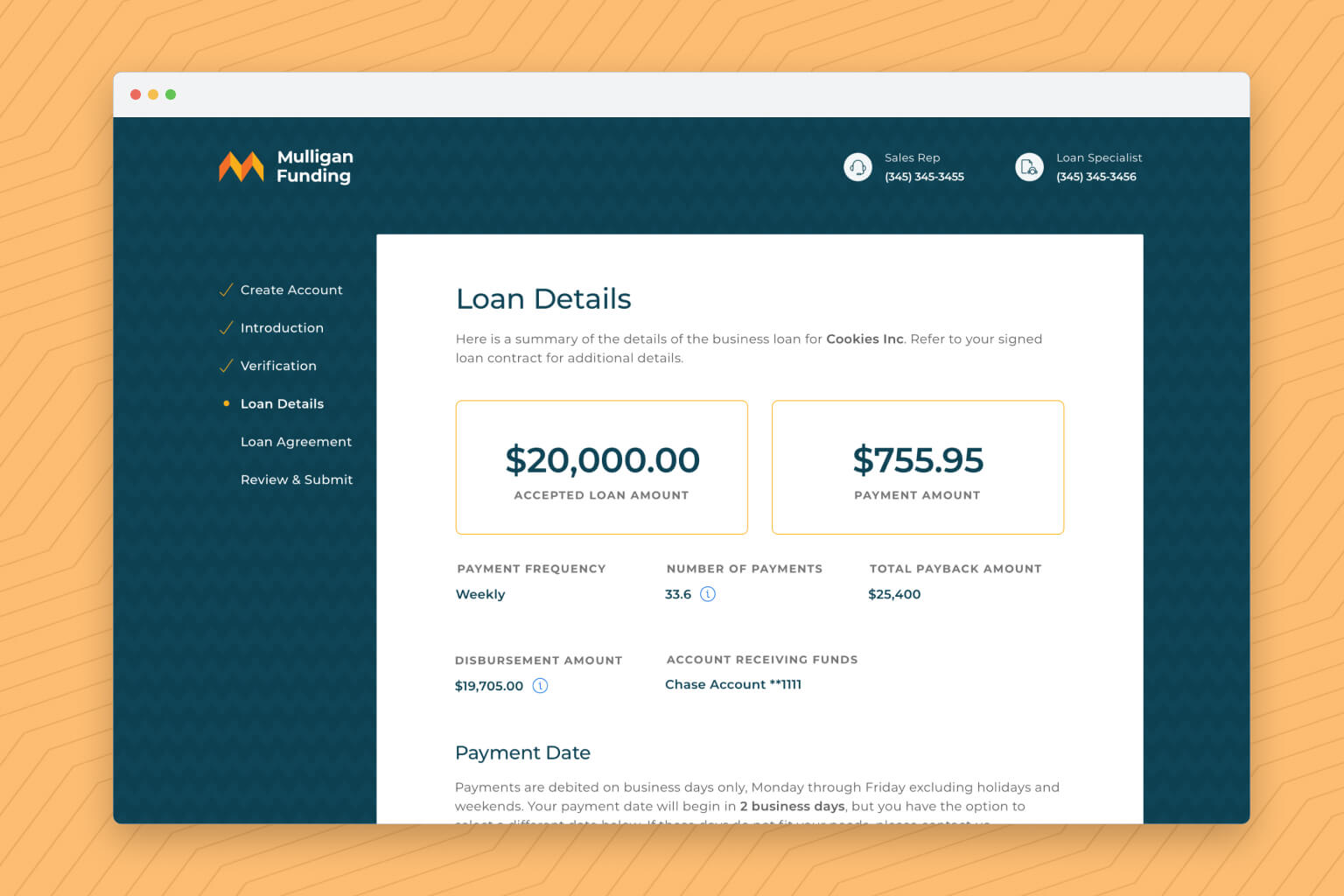

Reviewing Loan Details

Merchants can review their loan details such as loan amount, payment amount and payment date.

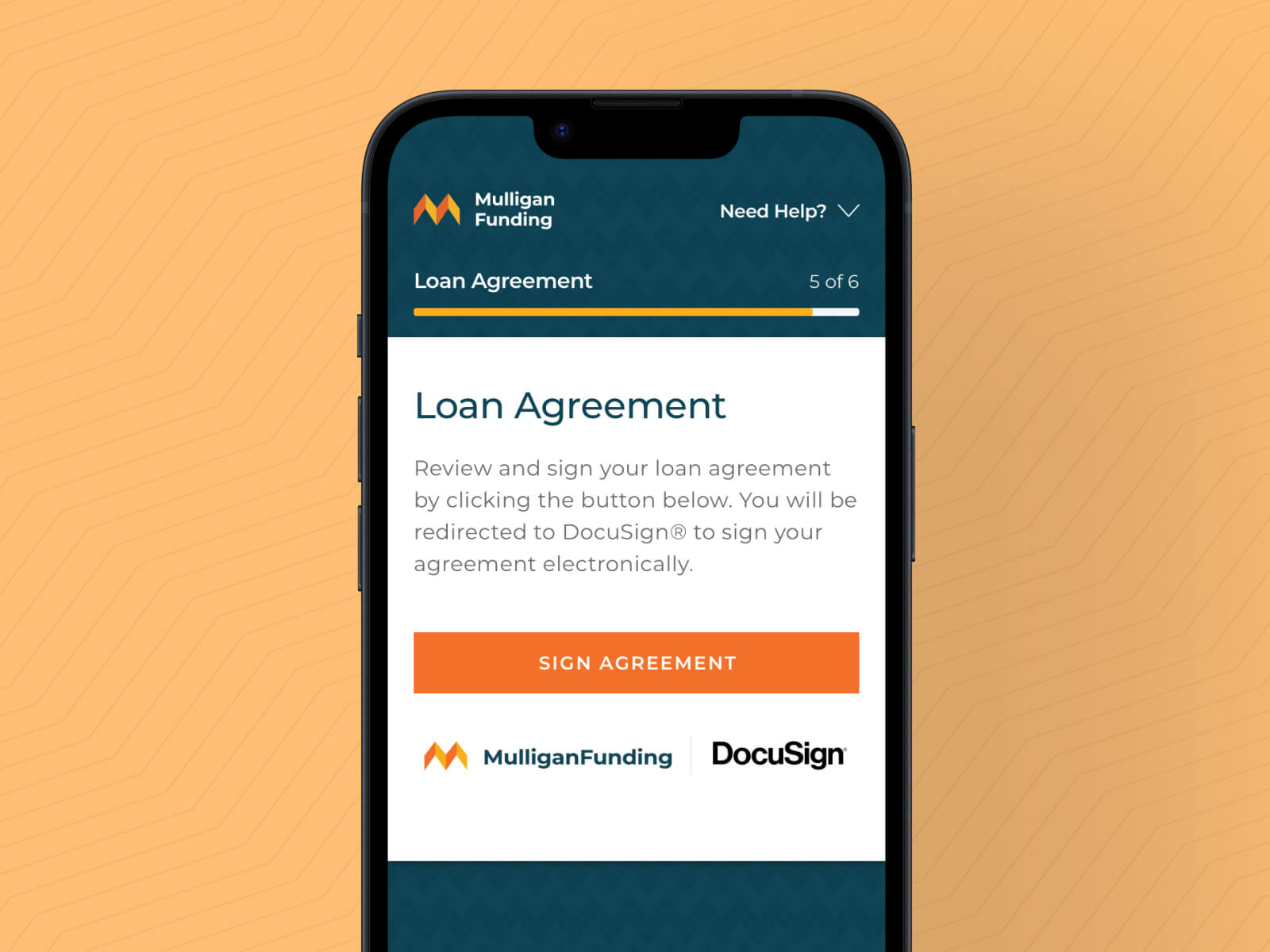

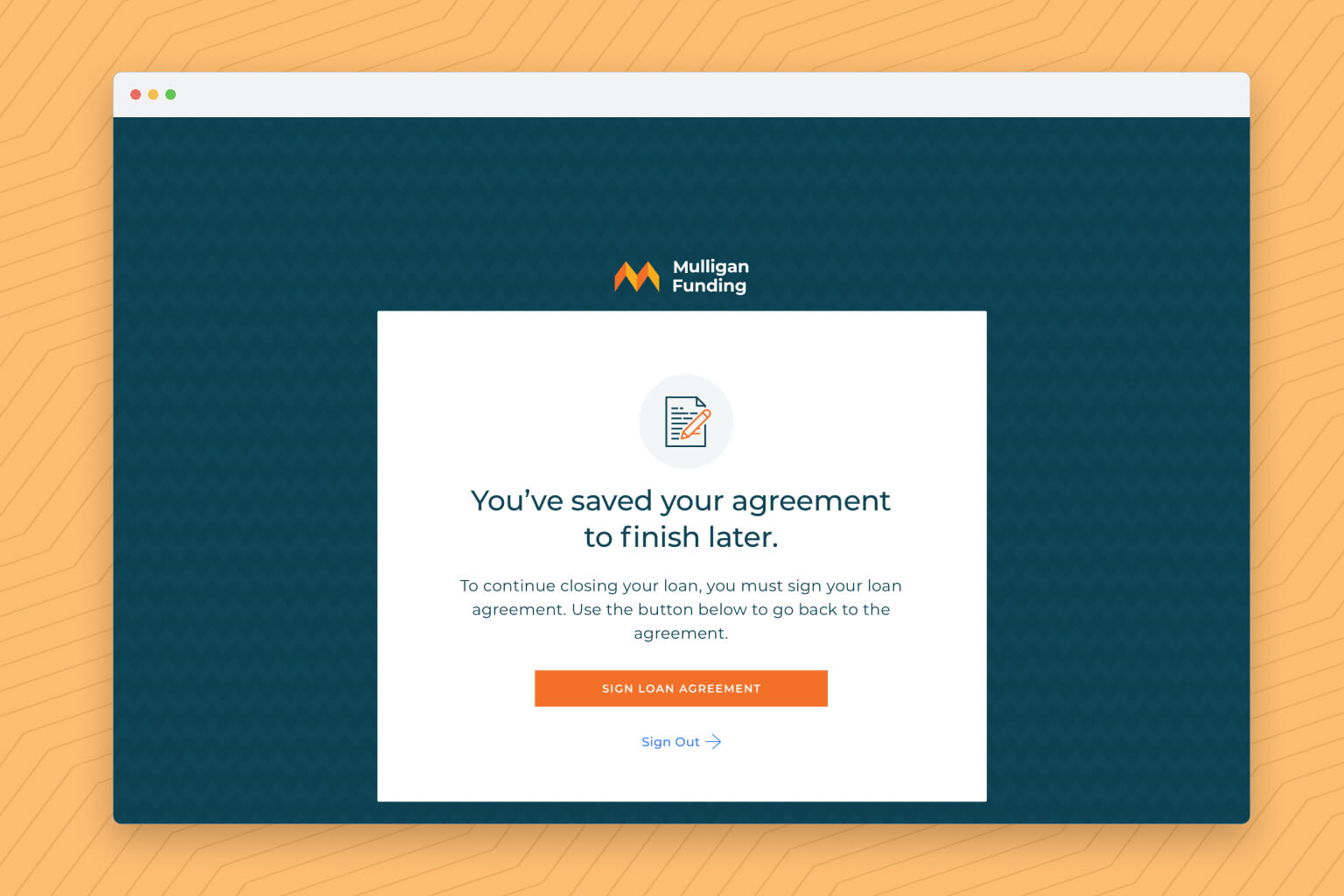

Signing Loan Agreement

If the loan agreement is not signed yet, merchants have the ability to sign and move closer to getting their loan funded.

Results & Impact

Documentation specialists have scheduled about 85% less closing calls. Calls are now only scheduled as a fraud prevention measure for riskier deals that need in-depth verification.

On average, merchants have completed loan checkout in about 6 minutes and based on client success feedback, merchants have found the experience to be convenient and mobile-friendly.

Our partnering brokers have enjoyed faster loan processing as now they are not dependent on a scheduled call to take place and can reach out to merchants to motivate them to complete their loan checkout.

Background

About Mulligan Funding

Established in 2008, Mulligan Funding serves as a provider of business loans and working capital loans to small and medium-sized businesses in the United States. Its mission is to provide a customer service experience that is seamless, transparent and allows business to feel confident they chose the right lender for their needs.

Discovery

Kicking Off The Project

I sat down with the COO and CCO to discuss the purpose of this initiative and the impact it will have. As there was no current online platform to finalize loan details, stakeholders were enthusiastic to get this project moving along and provide value to merchants and partners.

Currently, not having such platform has led to:

- Merchants not having an easy way to to review their loan details until they received their loan agreement, which usually comes after the verification call.

- Documentation specialists having to call all merchants to finalize loans. This created a large queue for the team.

- Partner's deal funding speed being slow as they have to wait for the welcome call. This sometimes deters them from sending deals with tighter turnarounds needed for funding. For context, partners are independent sales organizations (ISOs) that submit applications to Mulligan Funding and get a commission if funded.

Setting Up Goals

After discussions with stakeholders, the business and user goals were identified.

Business Goals

- Replace or at least reduce the time spent in the "Welcome Call" step done by documentation specialists

- Create a self-sufficient online experience for merchants to verify who they are and review their loan details prior to funding.

- Deliver a platform that can give Mulligan Funding a competitive advantage with partners to fund more deals through.

User Goals

- Ability to review loan details and identity without the need to directly be contacted.

- Sign and review loan documents.

Scope & Constraints

Taking Over An In-flight Project

It is important to note that this project had been started by a design agency and I took it over when I joined Mulligan Funding. They worked on some initial wireframes that gave me some understanding the direction Mulligan Funding was going with; however, as future iterations were reviewed, additional workflow updates had to be considered.

New Platform Constraints

As this initiative was the first external facing platform for merchants, developers had multiple research spikes to learn about how and what integrations needed to be built. Such spikes looked into account management, identity verification, Docusign (digital signature vendor), and further integration with our customer relationship platform. This all resulted in working closely with developers to determine additional userflows that needed to be considered.

Design Agency Handoff

Handoff from design agency was straightforward. A meeting was set with the agency in which we discussed what they had worked on. I was also given access to the Figma design file where they had started the wireframes as well as some initial concepts for responsive design.

Understanding How Things Work

Learning About the Internal Process

Because I was unfamiliar with the internal processes of the documentation specialists, I met with the Chief Credit Officer for an overview of what happens when an offer is sent out after underwriting. I learned that documentation specialists were responsible for making sure offer conditions were satisfied in addition to reviewing merchant information. As part of satisfying conditions, documentation specialists did a welcome call, where they verify the identity of the merchant and read the loan details. The need for the loan checkout platform was evident as these welcome calls took time from other essential responsibilities documentation specialists have.

Learning About Competitors

To understand a bit more about what Mulligan Funding wanted to achieve, I sat down with the VP of Sales to review a similar process from one of the competitors. This not only helped see the current standard for an efficient loan closing process, but it also served as an opportunity to ask about the competitor landscape in the small business lending industry. Being that I was new to the company, in fact, the first internal UX designer, I was able to get some context on the need to provide digital experiences for merchants and make our internal teams spend more of their time on key responsibilities. This conversation made it evident that this project was the start of big initiatives Mulligan Funding had planned.

Design

Design Principles

Based on the goals and priorities of this project, I focused on these 3 design principles:

Be Mobile Friendly

Allow merchants to accept loan terms and details from their mobile devices.

Be Easy To Use

Create a simple flow and guide users through their closing experience.

Be Secure

Verify the identity of the merchant prior to finalize loan details and signing the loan agreement.

Creating The Overall Userflow

After further discussing the requirements, I created a workflow to review the overall process from a high level. This became useful when it came to reviewing the vision with developers as it helped align what stakeholders wanted to achieved.

Identifying Key Solution Elements

The following key solution elements were identified and served as my top priority design checklist:

- Business & Identity Verification

- Loan Details Review

- Loan Documents Signing

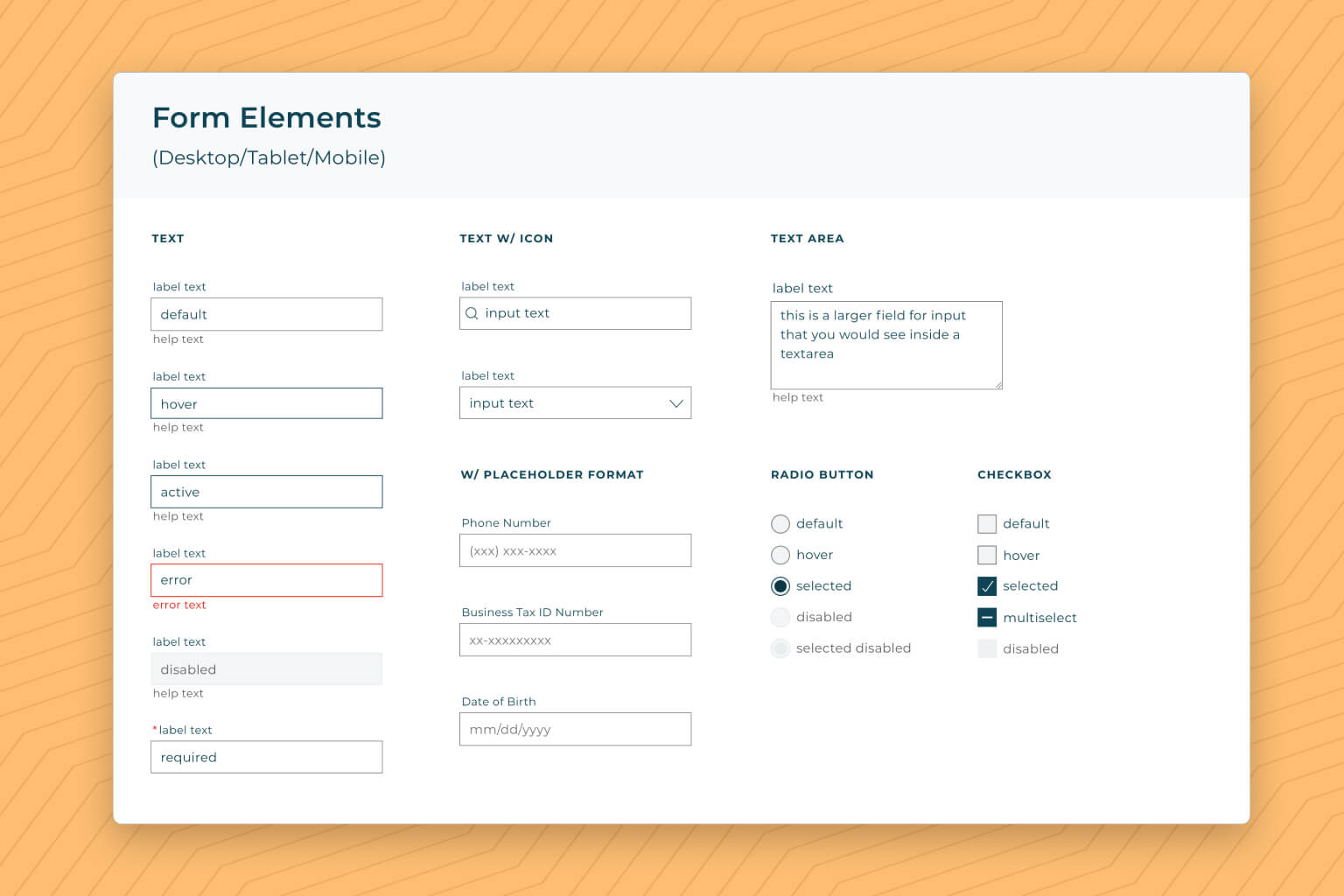

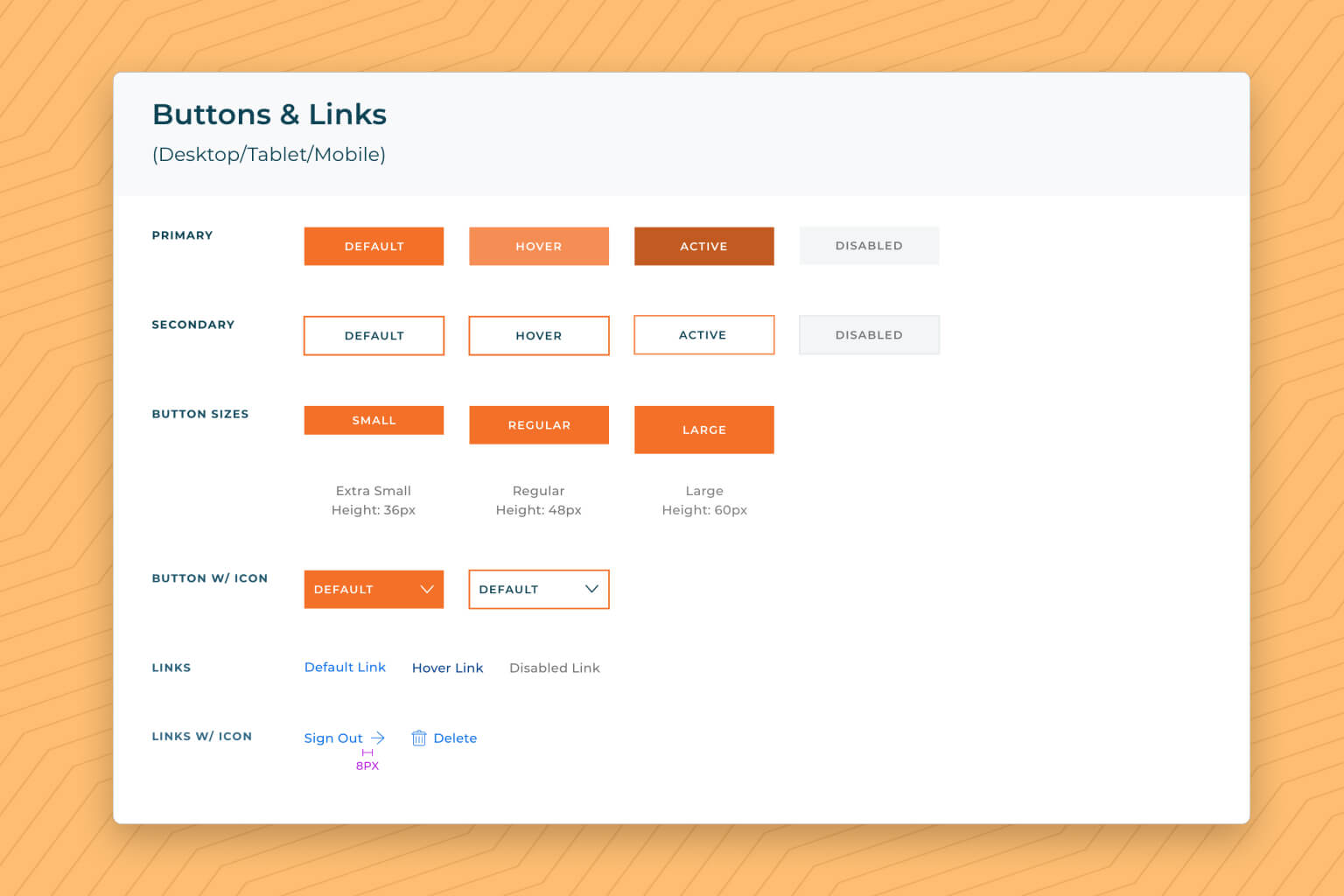

- Design System/Style Guide Creation

Feature: Business & Identity Verification

Focus: Be able to verify the business and merchant identity to be able to review loan details.

Business Verification Page

To verify an owner, the owner is asked to provide their business tax ID, date of birth, and the last 4 of their social security number. These fields were identified as essential by stakeholders and developers, allowing for a simple initial page.

Once verified, they are able to create an account which they can use to sign in and continue where they left off.

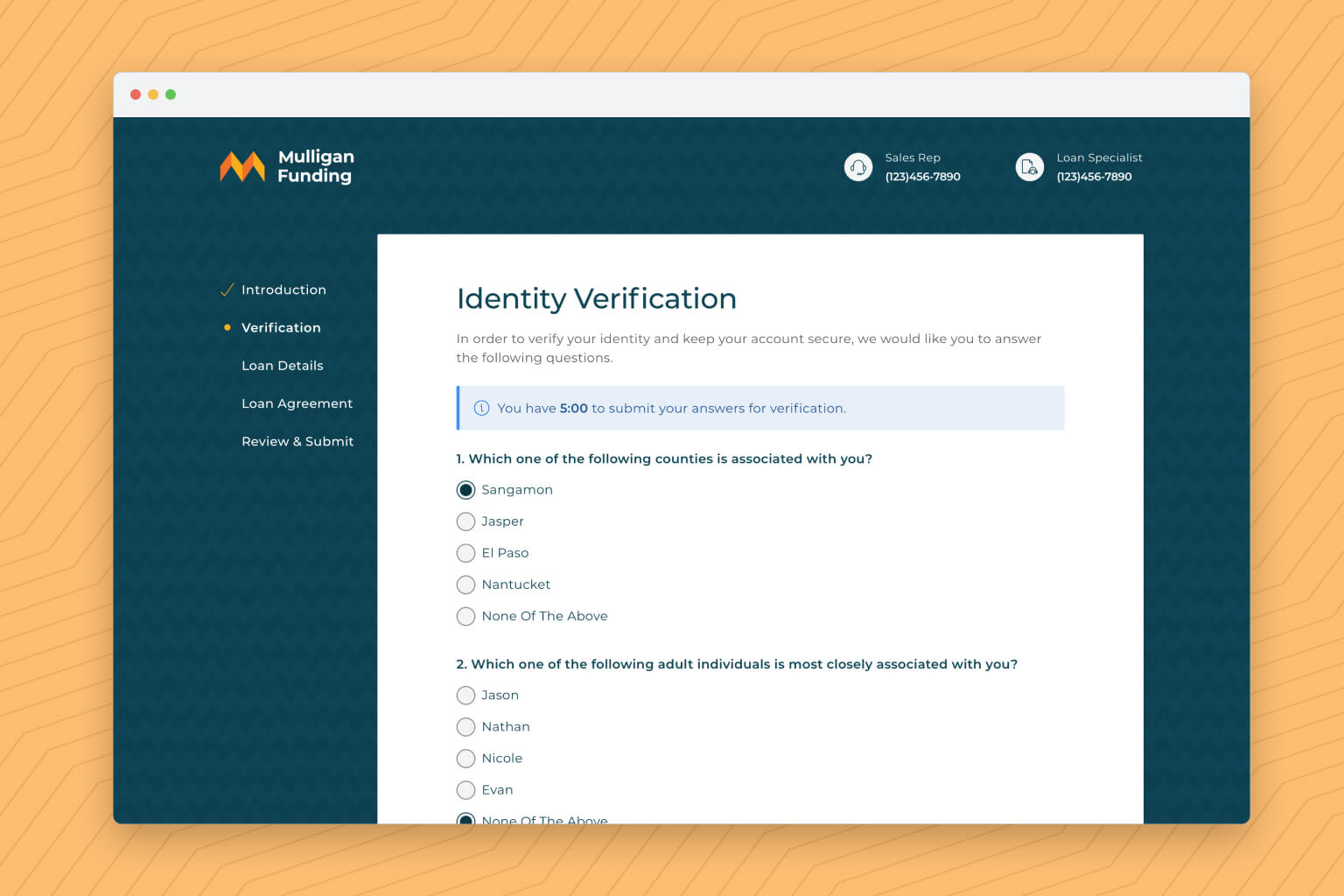

Identity Verification

An initial solution was the consideration of phone verification to authenticate the owner. Though this was a simpler form of verification, the following reasons were downsides that we needed to consider:

- The phone under the contact might not be a primary contact in their phone service

- Phone number provided might be a phone number used by the business, such as a landline and the text message verification method would not work.

An alternate solution was a more traditional method by asking questions obtained from public records. This method created more friction for the user as they had to answer a randomized set of 5 questions. Nonetheless, this method provided high level of confidence that the person finalizing their loan details is the user who initially verified the business. This ended up being the selected solution.

Feature: Reviewing Loan Details

Focus: Allow users to review loan information and agree to terms & conditions

Perhaps the most important feature of this initiative, reviewing loan details required great attention. The most important numbers to show were loan amount and loan payment with a few other details highlighted.

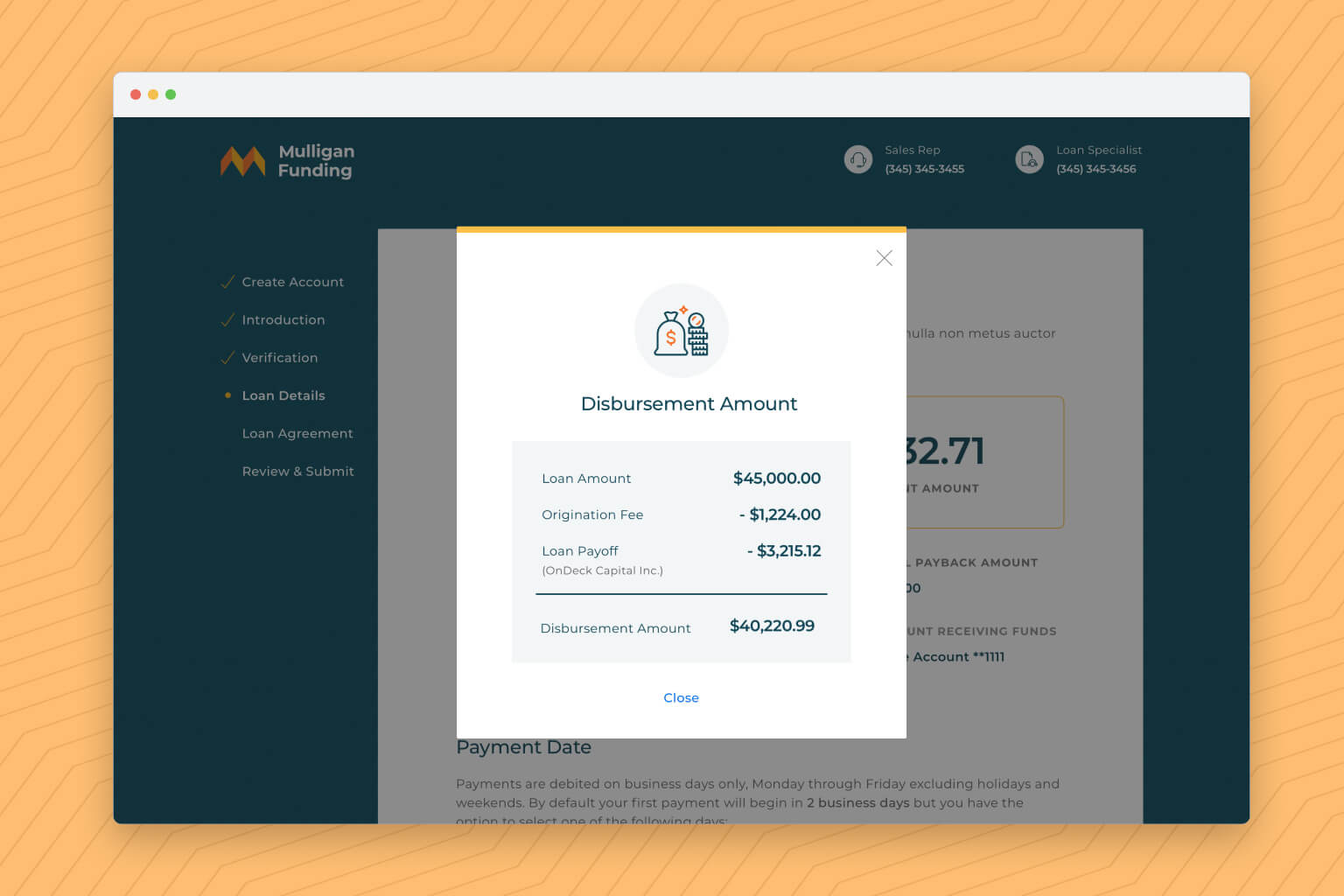

Providing Tooltips

It was also important to explain some terms for merchants. A simple solution for this was to implement tooltips that trigger informational modals. This way, merchants had the option to select them if needed while maintaining a non-intrusive design.

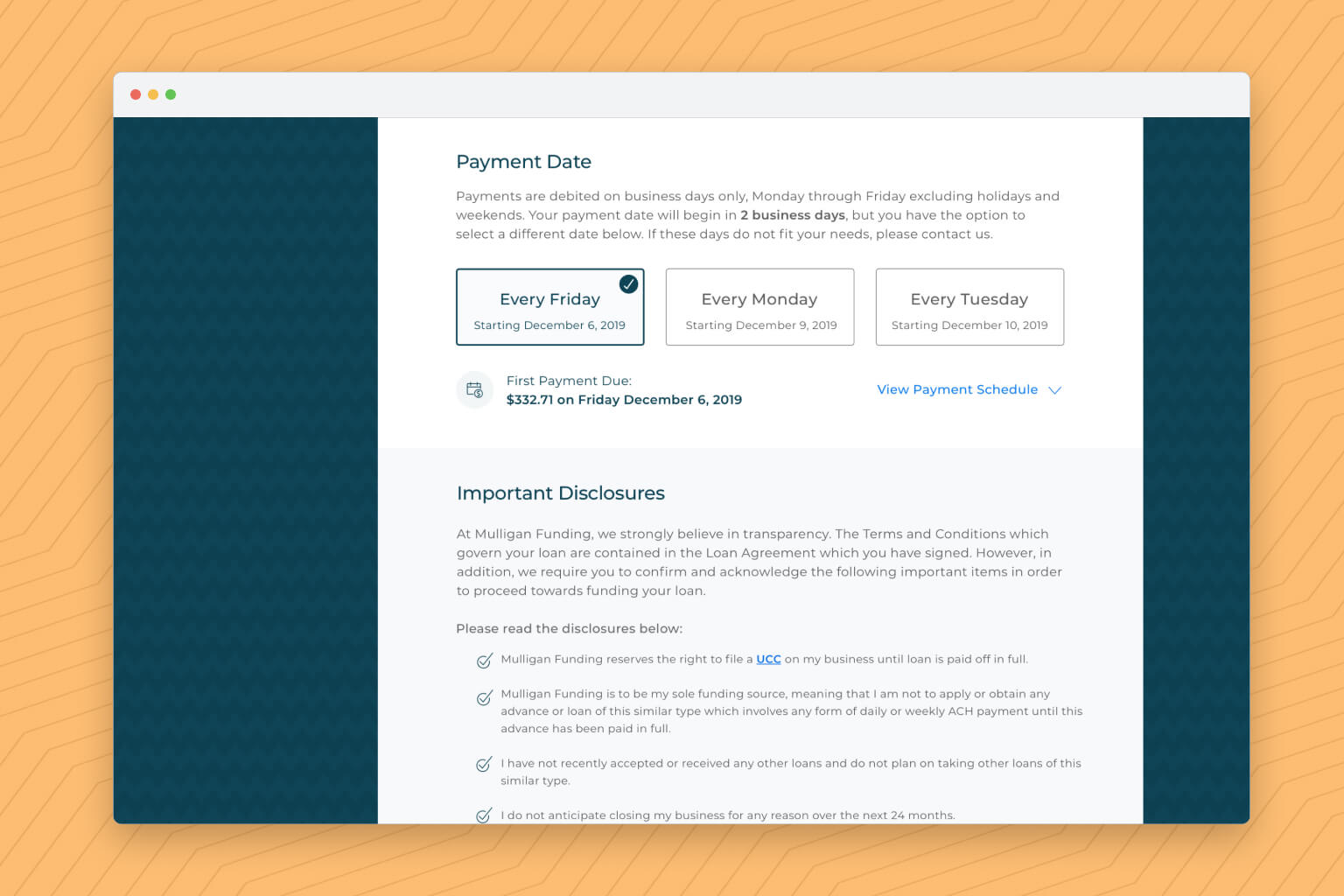

Selecting Payment Day

Allowing merchants to select a payment to start paying off a loan provided a sense of flexibility up to their discretion. This only impacted loans with daily payments and days were limited up to 3 business days in advance.

Showing a Payoff Table

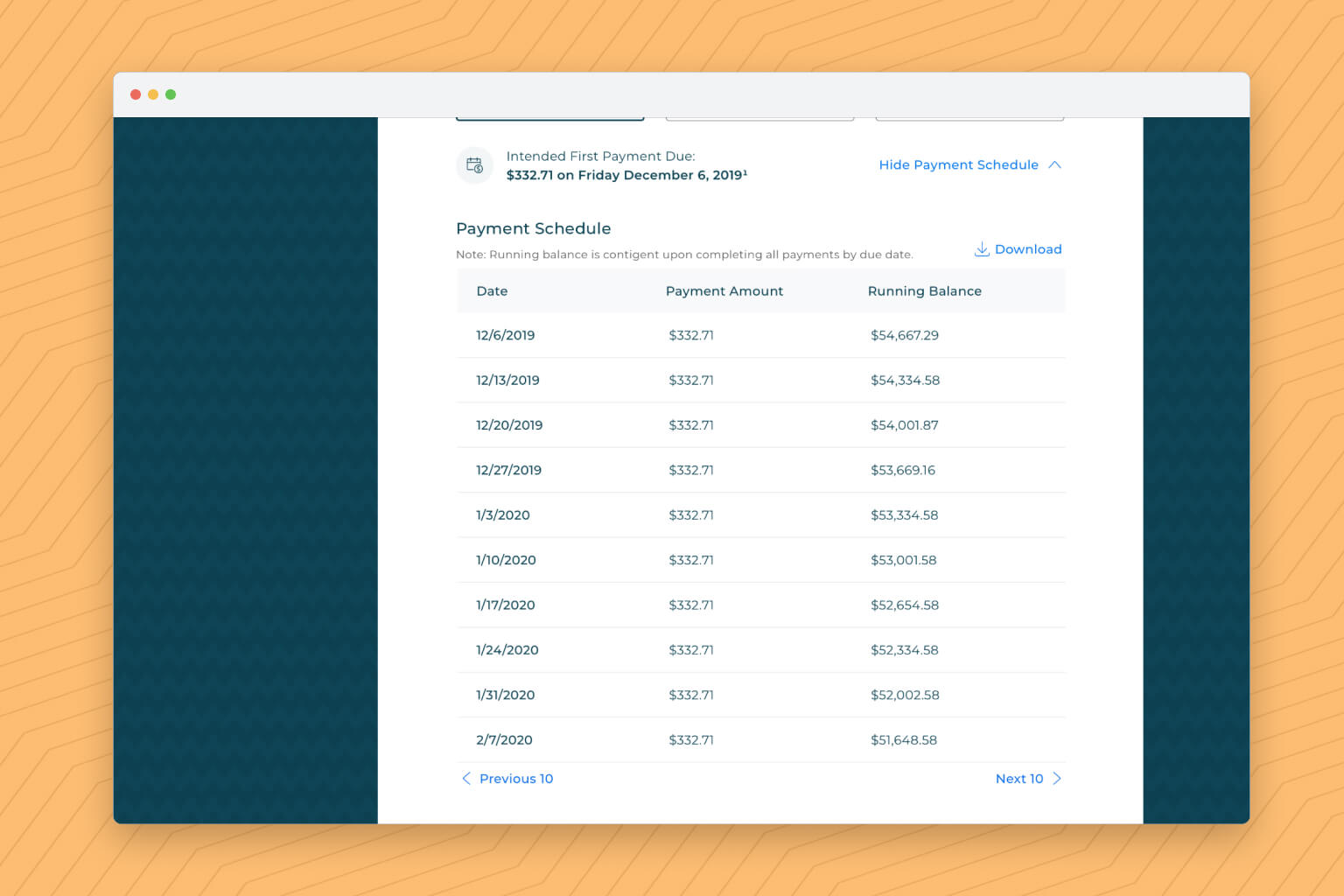

Merchants also got an estimated payoff table from their payment date with the assumption of fixed payments throughout their loan. This was useful for merchants to get an idea of how much they will have to paid by a certain time. An option to download as a spreadsheet was also implemented.

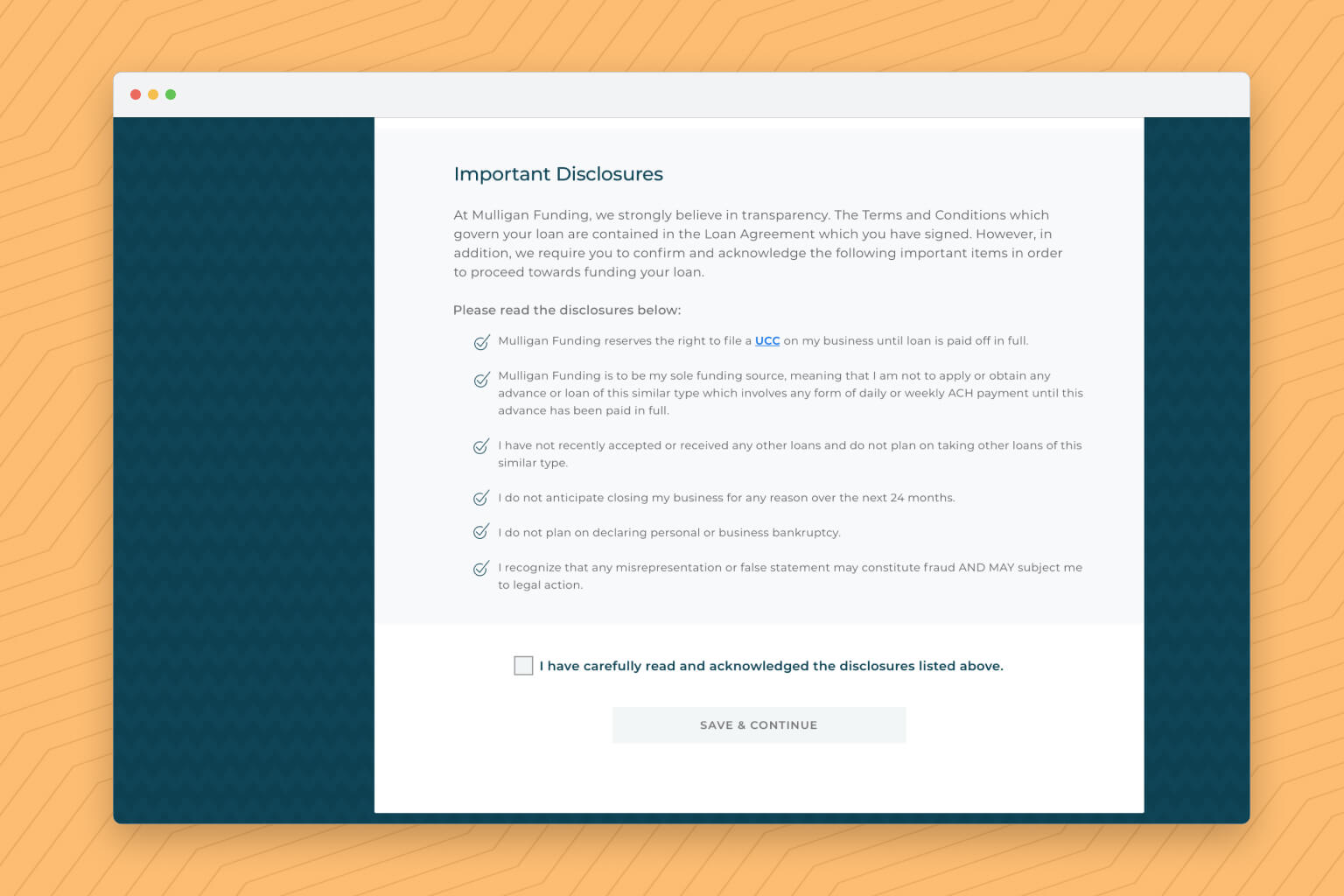

Reviewing Terms & Conditions

Initially this section was omitted from early designs but it was important for the business to bring out important terms from the loan agreement for the merchant's visibility. The business needed an active acknowledgment so a checkbox was implemented for agreement. Convincing the stakeholders to have 1 checkbox instead of multiple to satisfy this requirement was a big win for the experience as this kept it simple for the user.

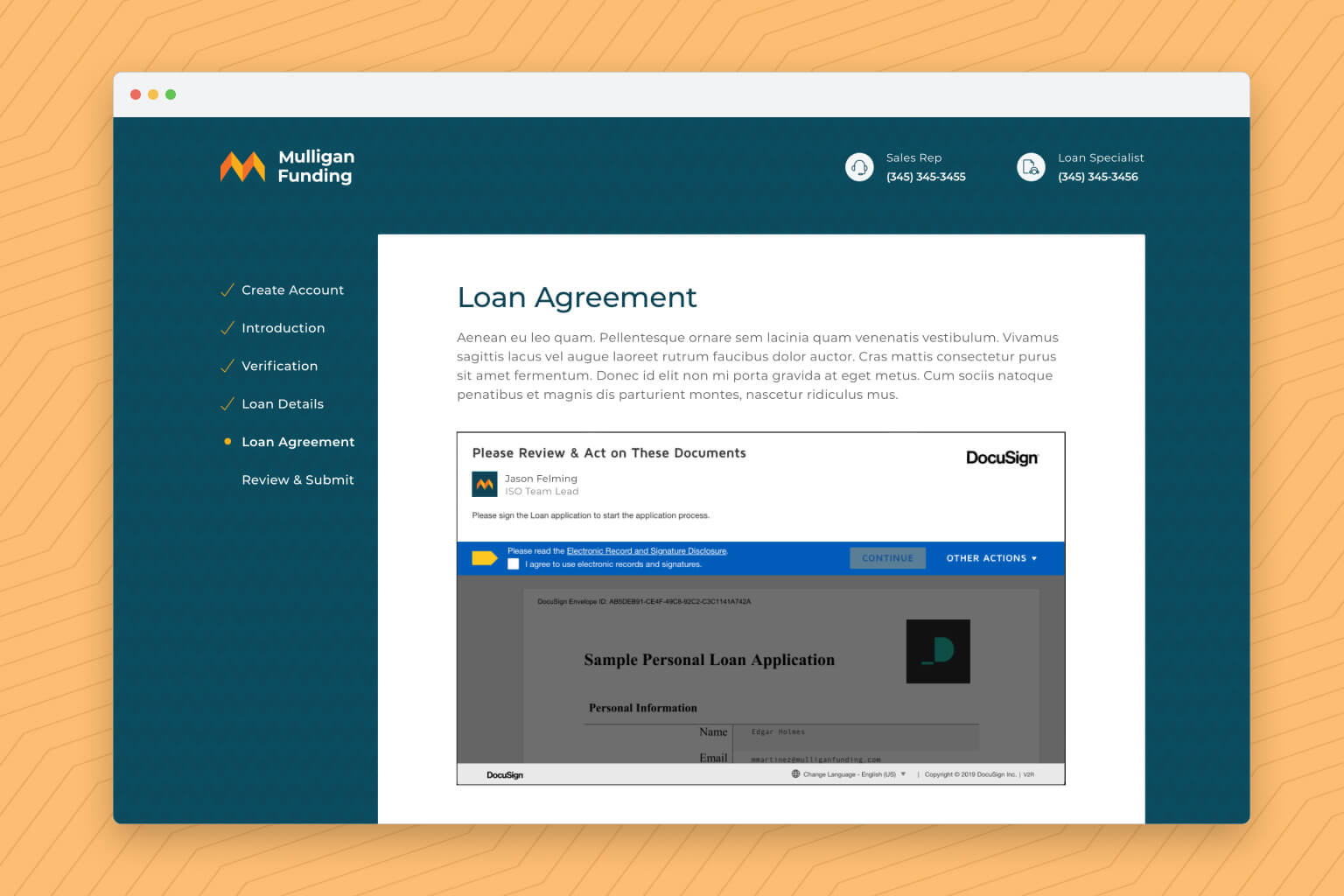

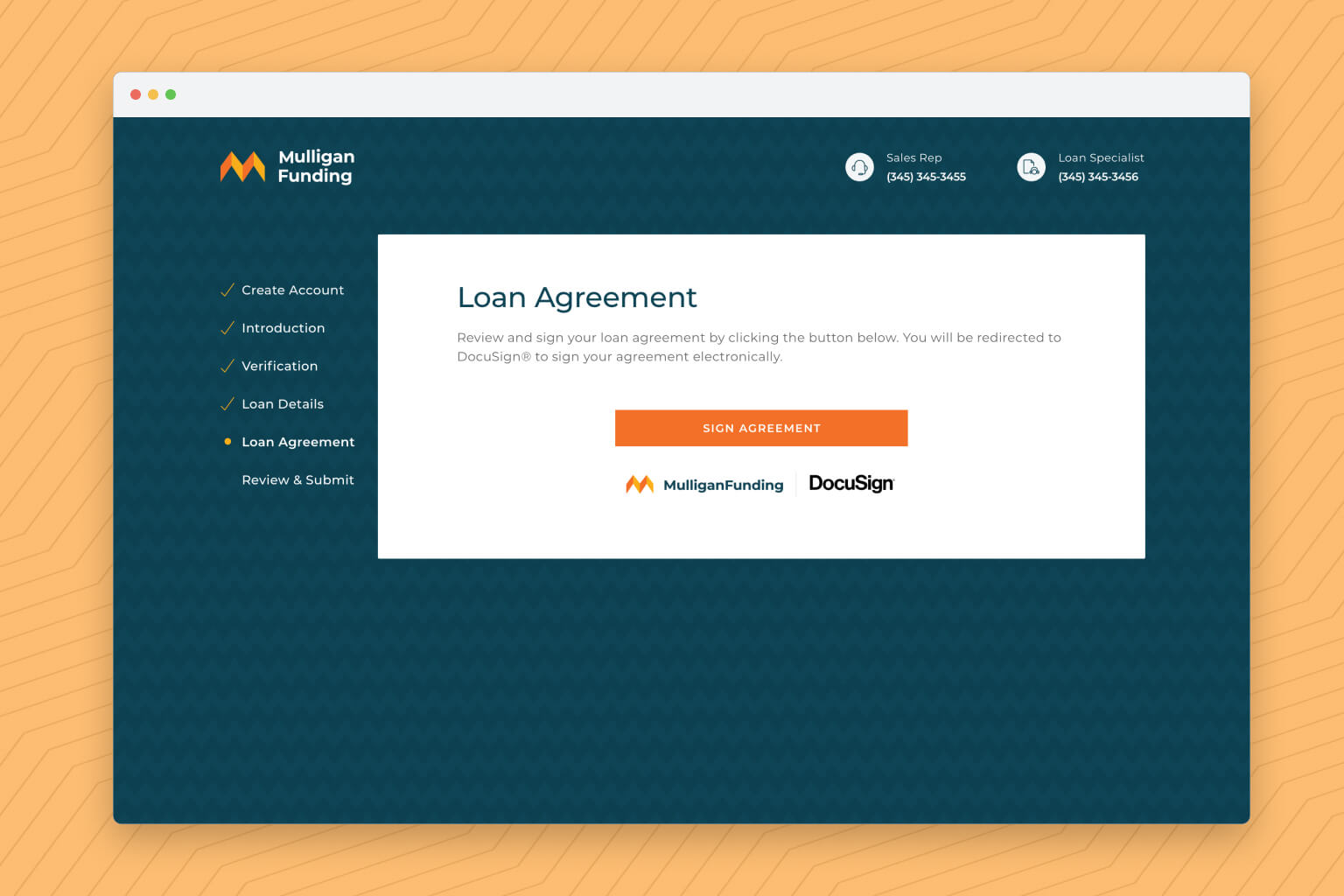

Feature: Signing Loan Documents

Focus: Sign loan documentation through an electronic signature (Docusign)

One thing that was added midway through the project was the need to include a digital signature capture step. It was determined that this would create value for merchants as they would be able to sign their loan documents within this closing process instead of waiting for an email or call. This increased the scope of the project, as now we had to consider implementation of the vendor and any additional use cases. For context, Docusign is the current digital signature platform used and was kept for internal processes consistency.

Iframe Ideation

- One of the explorations included an iframe implementation within the loan checkout experience. However, because a trigger is needed to start the Docusign process, developers found it easier to create a button that would redirect the user to Docusign. Once signed, they were redirected back to the platform.

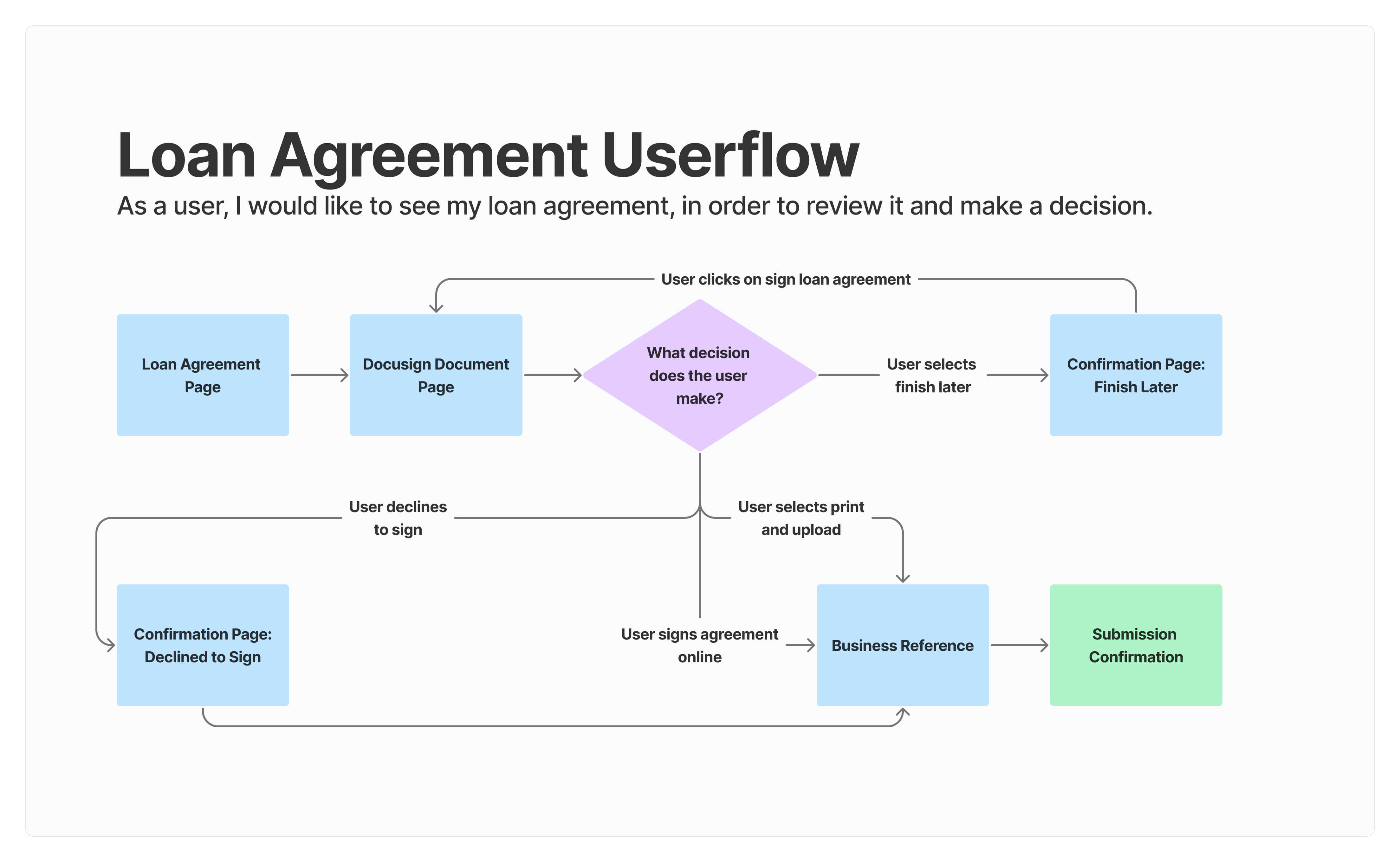

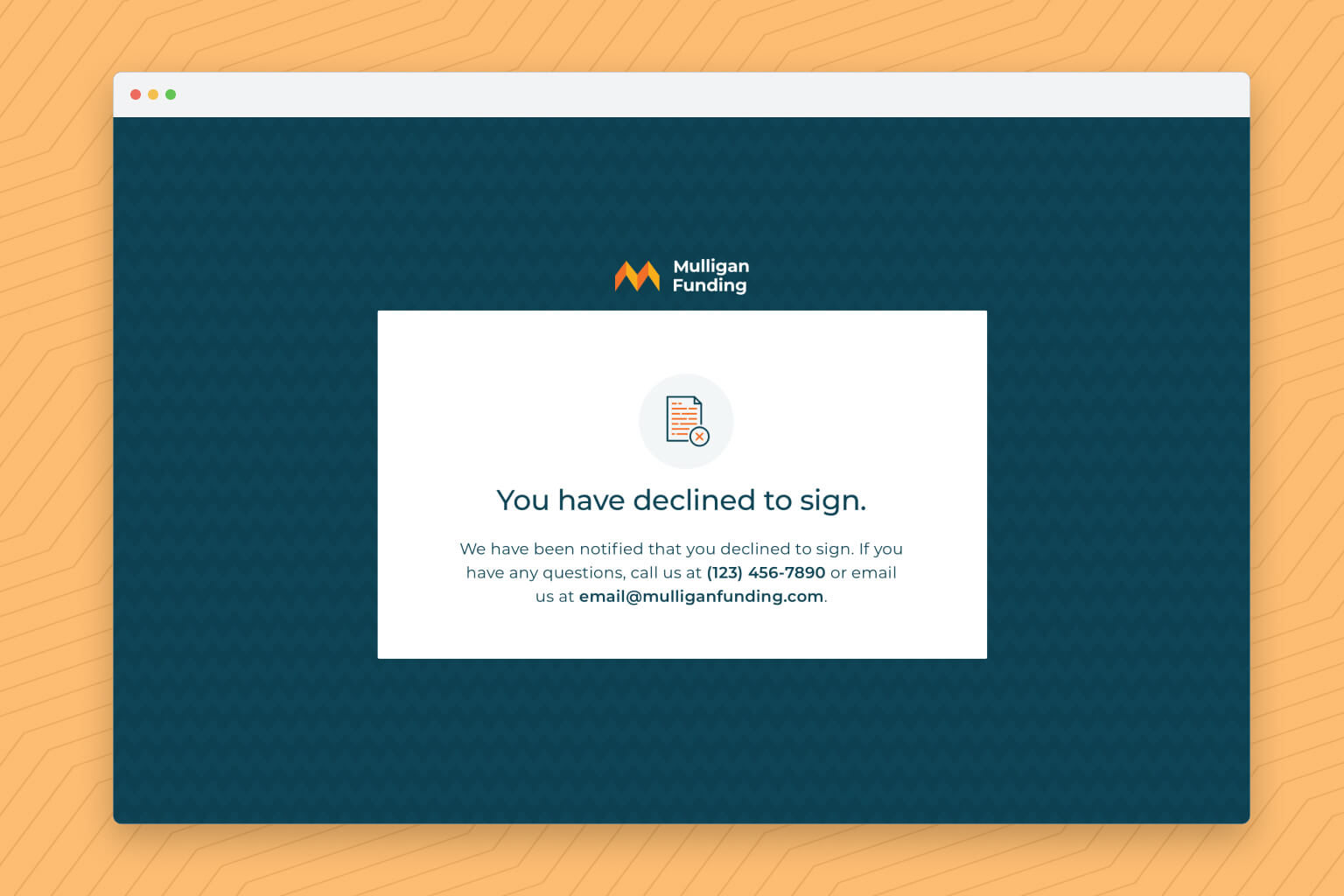

Challenge: Considering Different Scenario Decisions

Multiple Docusign decisions needed to be considered for a proper implementation with the platform. Some scenarios that needed to be considered were:

- If a user select on sign later

- If a user declines to sign

- If a user selects print and upload

To help identify such scenarios, I met with documentation specialists to understand the multiple stages of loan documentation. This helped confirmed if there were some scenarios missing in my initial testing of the Docusign document signing process.

A list of Docusign agreement states was created to cover all the statuses prior to signing and submitting.

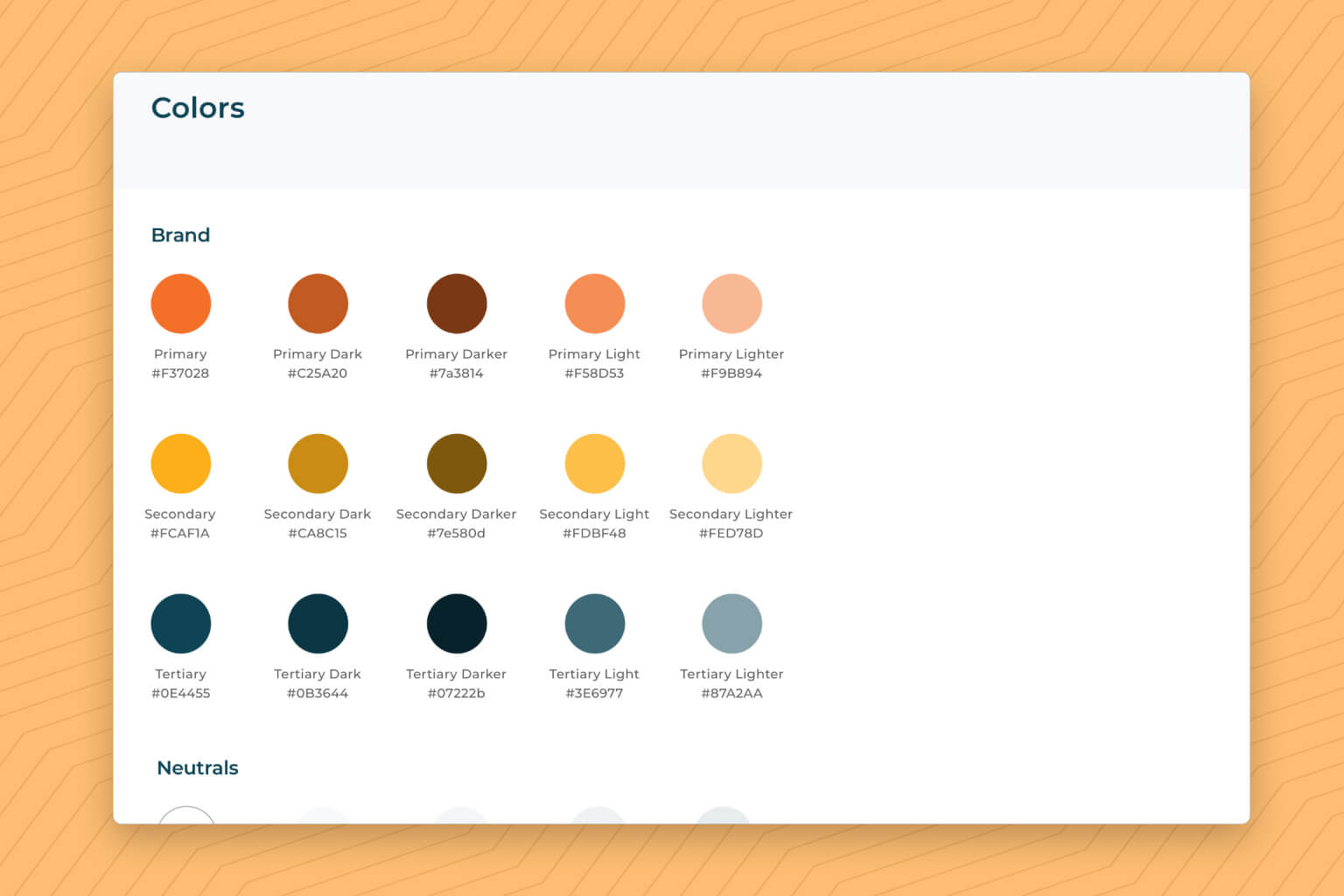

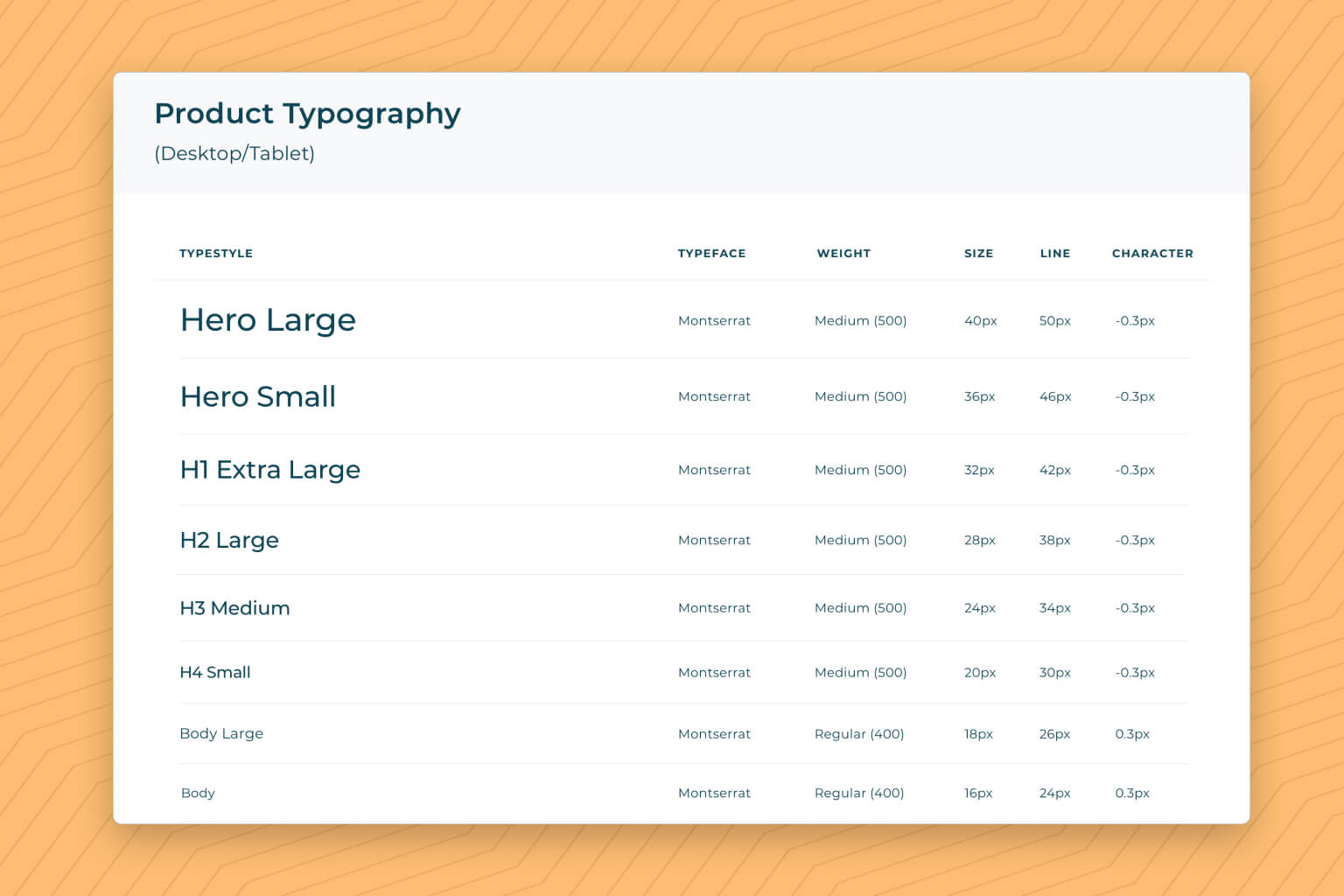

Creation of Style Guide & Design System

Focus: Creation of design system with fundamental elements and components

As the first internal designer, I made an effort to create foundational elements of a design system for future use. At the same time, I took this opportunity to create a design library to make reusable elements, styles, and colors within the Sketch app. This became extremely helpful during iterations of designs as well as when the UX Lead was hired a few weeks later.

Delivery

Collaboration For The Win

Developer Reviews

Design reviews were very smooth for this project. I met with developers throughout the design process to ensure they understood my designs and allow them to ask any questions. These meetings also helped with alignment as I had assumptions on integrations and I modified my designs accordingly based on their feedback.

Developer Hand-Off

As I was meeting with the development team often, hand-off was straightforward and easy. I created assets for icons and illustrations in additional to tablet and mobile responsive designs. As I was fairly new to the development team, I made an extra effort to make myself available with any questions they had with the prototype or the assets provided.

Helping with Quality Assurance

During this time, the technology team started expanding and a new QA engineer was hired; however, they had low capacity as current internal platforms for loan funding had priority. Knowing this, I offered some help finding UI issues and performed some mobile responsiveness testing. A document was created with the issues found, organized with a design priority and overall importance.

User Impact

Partners (ISOs)

The impact of this new self loan checkout platform was felt immediately. Our partners were ecstatic that Mulligan Funding finally had this service as it facilitated their loan processing by reducing time it takes for merchant to sign documents.

Documentation Specialists

Internally, documentation specialists began spending more time on fulfilling offer conditions for deals. It is important to note that the Welcome Call was not fully removed from their process as they still perform a welcome call for deals that are considered risky. Essentially, welcome call has become a preventative measure from fraudsters and only used as needed.

Merchants

Based on conversations with the customer success team, the team mentioned that most merchants enjoyed the self-serving experience and were glad that help touch points were made available by having a phone number they can contact. Shoutouts were also given for making the experience super mobile-friendly.

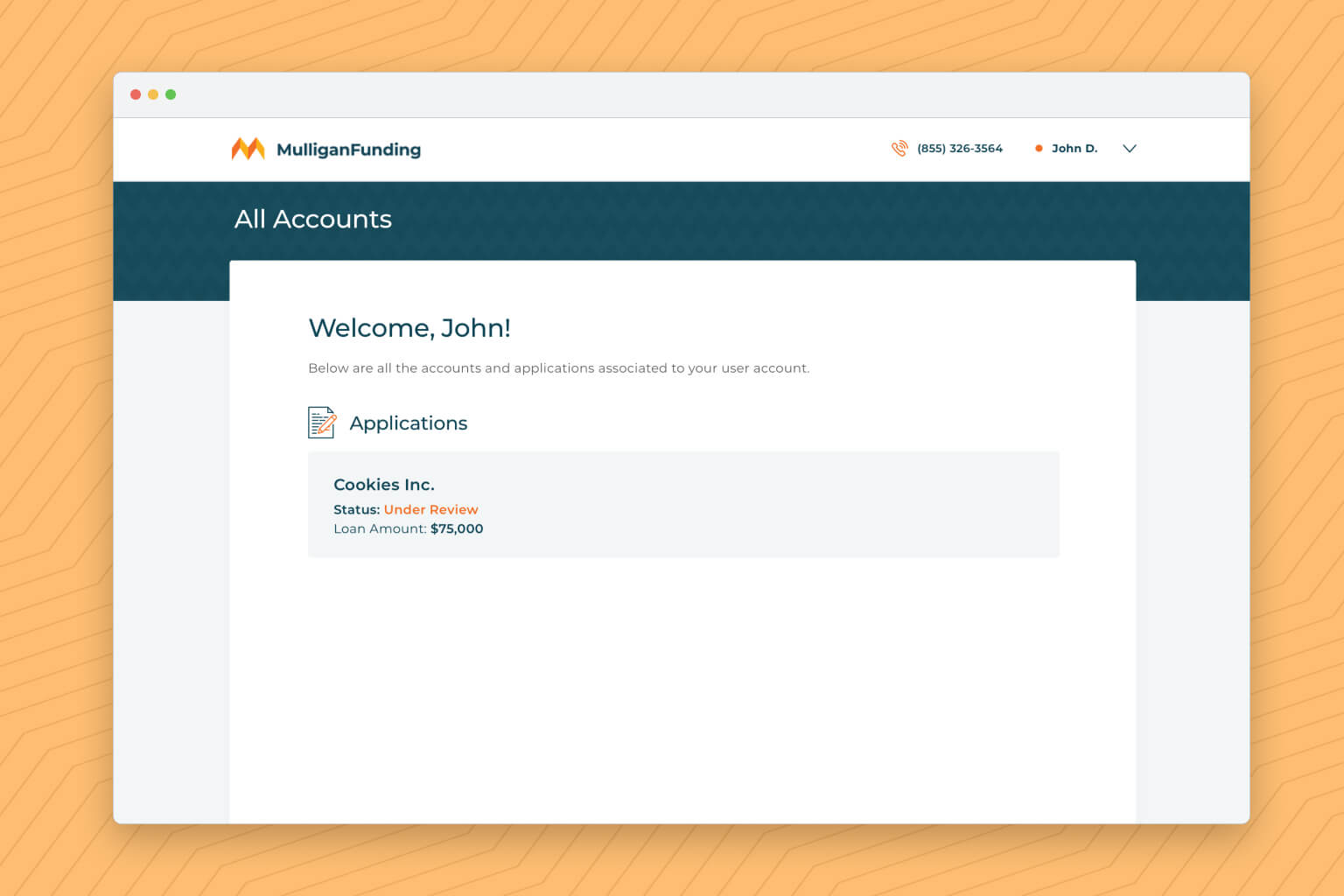

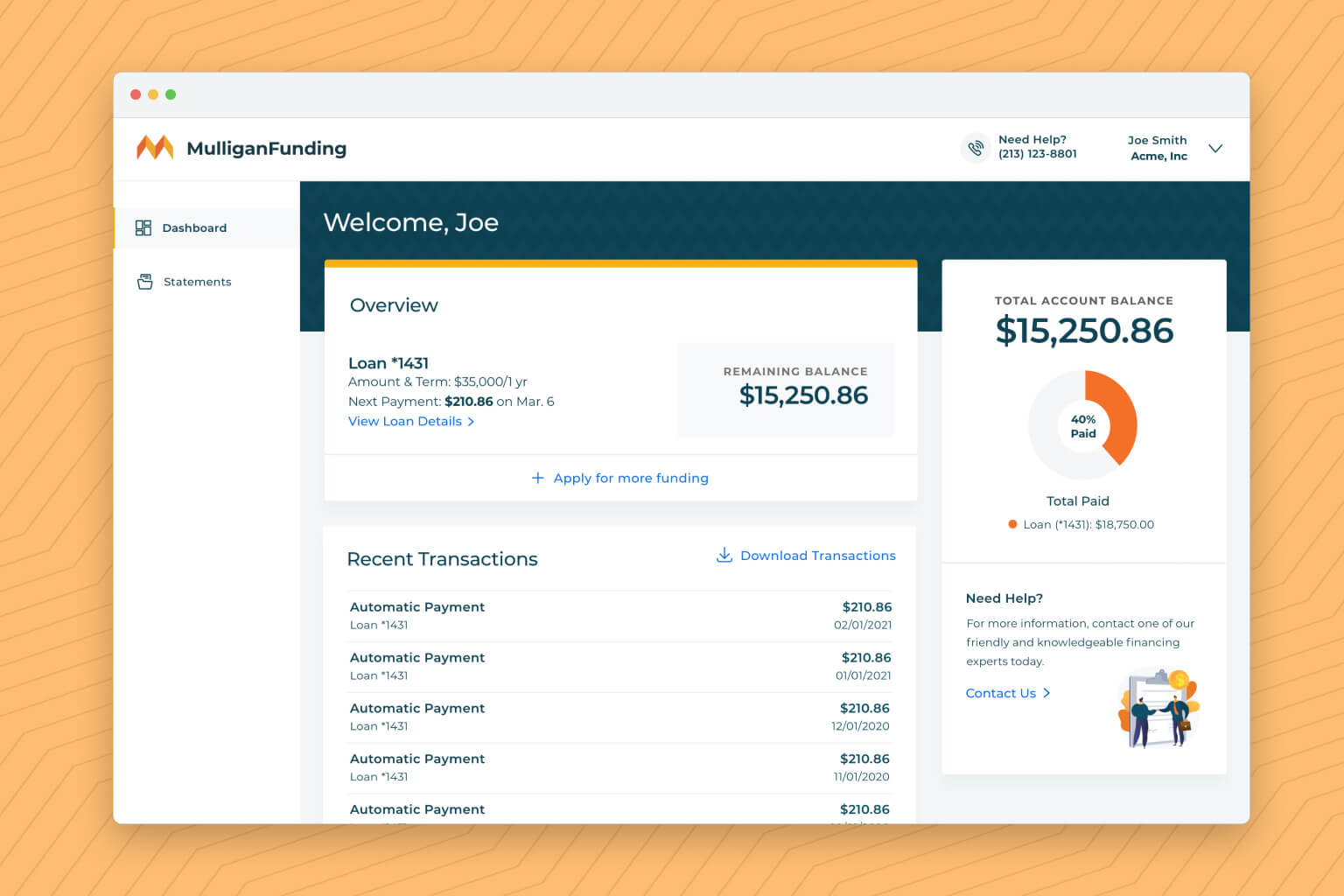

Next Steps

Thinking What happens After Closing

Something that was not expanded upon in this case study was the experience after a merchant finishes their loan checkout experience. As of now, once their loan is funded, they are taken to a minimal overview page, where they can see some basic information about their loan as well as obtain a second loan once they are eligible.

It is evident based on the above design, that this overview page can be improved on as it was design with the intent to built a customer portal experience down the line. A full customer portal experience has actually been designed; however, due to the current business goals and needs, it has not been prioritized yet.

Conclusion

Takeaways

Cross-Functional Team Collaboration

Collaboration was extremely important for this project, specially because of the fast-paced iterations due to the delivery date set early on the project. This gave the project a sense of "all hands on board" to meet the deadline and everyone made an effort to move it along.

Taking Initiative

Being that Mulligan Funding had a small technology team during those days, specially not having a full-time product manager hired, it was important to take initiative and finding answers. I made an effort to understand the internal processes of funding a loan just to get a high level idea of the business model we had. Lastly, it also became clear the importance of having support when taking initiative. The COO trusted me to figured out some things and helped me when I stumbled upon blockers.